Ask Pulse Ai

Services

Knowledge Hub

Resources

Tools

Ask Pulse Ai

Services

©PropTech Pulse 2025, All rights reserved.

In the financial landscape of April 2026, the housing sector continues to benefit from a period of notable stability. With the Reserve Bank of India (RBI) maintaining the benchmark repo rate at 5.25%, lenders have held lending rates steady, providing a predictable environment for prospective homeowners. For those entering the market, this stability creates a strategic window to compare offerings and secure favourable terms before committing to a long-term mortgage.

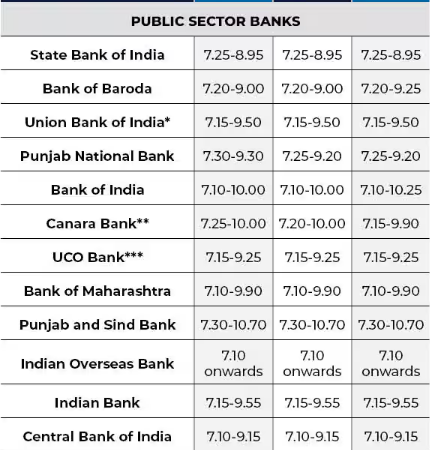

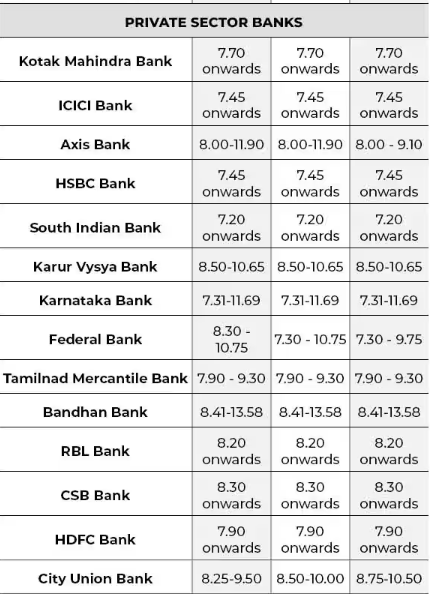

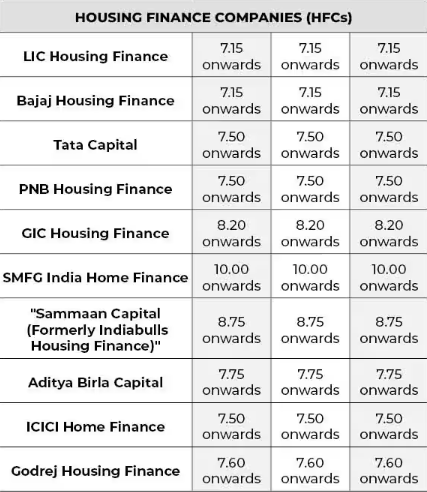

The Landscape of Competitive Rates

Market data for April 2026 indicates that competitive home loan interest rates start at approximately 7.10% per annum, particularly among public sector banks. While headline rates provide a starting point, borrowers must look at the "spread", the margin a lender adds, which fluctuates based on the applicant's risk profile. It is essential to look beyond the base rate and evaluate the total cost of borrowing, which includes varied processing fees and administrative charges.

Strategic Variables for Loan Approval

Lenders are currently applying a rigorous multi-layered evaluation process to mitigate risk. Your CIBIL score remains the "golden threshold"; maintaining a score of 750 or above is critical to accessing the lowest interest brackets. Beyond credit history, lenders are scrutinizing the Debt-to-Income (DTI) ratio, with experts advising that your monthly EMI obligations should not exceed 40% of your net income to ensure financial resilience and loan approval.

Leveraging Loan-to-Value (LTV) Ratios

A proactive approach to your down payment acts as a significant leverage tool in loan negotiations. The Loan-to-Value (LTV) ratio, the portion of the property value financed by the bank, is a primary driver of the interest rate offered. By opting for a larger down payment, you effectively reduce the lender's risk exposure, which can often be used to negotiate a lower interest rate and potentially secure waivers on certain processing fees.

Fixed vs. Floating Rate Dynamics

The choice between fixed and floating rates in 2026 continues to be a central decision for borrowers. While fixed rates provide insulation against sudden market shifts, floating rates - linked to the Repo-Linked Lending Rate (RLLR), remain the preferred choice for many, as they allow for the immediate transmission of any potential future rate cuts by the central bank. Assessing your personal risk appetite is key to deciding which structure aligns with your financial future.

Conclusion: Securing Long-Term Stability

Taking a home loan is a significant financial commitment that demands a data-driven strategy. By focusing on your credit health, maintaining a manageable DTI ratio, and thoroughly comparing lenders, you can ensure that your home remains a sustainable asset. As the market remains stable in 2026, prioritizing long-term financial sustainability over the lowest headline rate remains the most prudent path for homeowners.

Unlock the Latest in Real Estate

News, Infographics, Blogs & More! Delivered to your inbox.