Ask Pulse Ai

Services

Knowledge Hub

Resources

Tools

Ask Pulse Ai

Services

©PropTech Pulse 2025, All rights reserved.

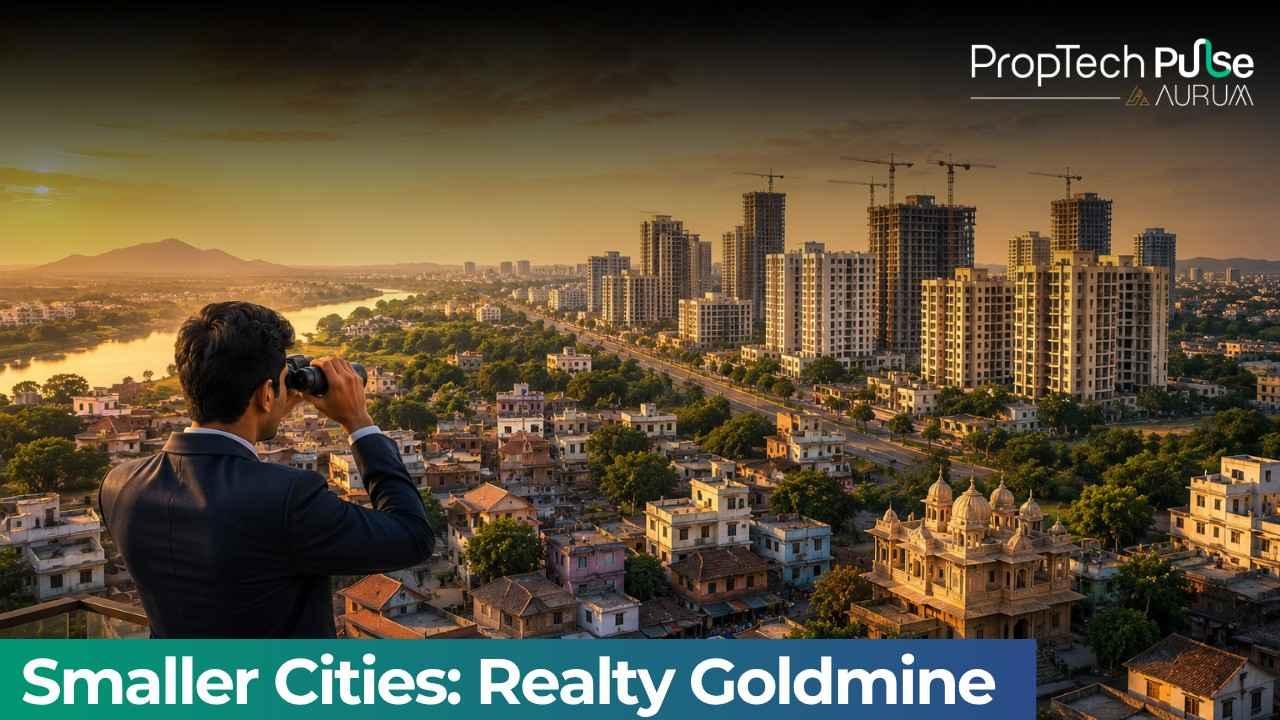

India's real estate narrative is no longer confined to the traditional boundaries of its mega-metros. In 2026, Tier II and Tier III cities have emerged as the "next premium real estate goldmine," signalling a profound structural shift in the country's urban investment landscape. This transformation is not merely a search for cheaper alternatives; it is a strategic, infrastructure-driven premiumisation cycle. As established metros deal with saturation, pollution, and high costs, smaller urban centers are becoming self-sustaining economic hubs, attracting both institutional capital and aspirational homebuyers.

Key Drivers: Policy and Infrastructure Renaissance

The foundation for this growth was reinforced by the Union Budget 2026–27, which emphasized high-speed rail connectivity, metro expansions, and upgraded civic facilities for cities with populations above 5 lakh. These developments have unlocked entirely new real estate micro-markets, with micro-markets near expressways and freight corridors registering accelerated price discovery. Analysts at KPMG India note that project land prices in these regions are projected to rise between 25% and 100% over the next few years, directly linked to their evolving status as regional economic hubs.

Premiumisation Over Affordability

A major misconception is that smaller cities are growing primarily because they are affordable. On the ground, the biggest driver is actually premiumisation. In cities like Coimbatore and Mohali, more than half of all new sales in top locations are now for homes priced above ₹1 crore. This shift is validated by data from Magicbricks, which projects India's luxury housing market to grow at a CAGR of 35% through 2030. Buyers in these markets are increasingly prioritizing:

- Quality of Life: A quest for clean living, open spaces, and reduced traffic congestion.

- Design and Amenities: Growing demand for integrated townships, branded residences, and amenity-rich developments.

- Global Exposure: Aspiration-driven consumption fueled by rising household incomes and exposure to international living standards.

The Performance of Rising Hubs

The growth is concrete and visible in capital appreciation rates across specific cities. While Delhi’s average price growth remains moderate, Kanpur and Lucknow have recorded year-on-year growth of 24.53% and 22.61% respectively. Lucknow alone has delivered over 80% appreciation since 2019. Other cities reinforcing their positions as high-potential residential markets include Indore, Nagpur, and Jaipur, while emerging corridors in Bhubaneswar and Raipur are gaining momentum as the next phase of investment frontiers.

Future Outlook: A Multi-Nodal Growth Story

The 2026 market reflects a convergence of government policy, remote work flexibility, and regulatory transparency via RERA, which has built significant buyer confidence in smaller markets. These cities are no longer just "upcoming" destinations; they are delivering established returns and redefining how India builds its next layer of urbanization. With the temple economy fueling growth in holy cities like Ayodhya and Varanasi, and IT clusters expanding into Mysuru and Kochi, the future of Indian real estate will be defined by its ability to create premium living hubs across a geographically diverse landscape.

Enjoyed this update? Visit PropTech Pulse for more real estate news and market insights.

Ask Pulse Ai anything about real estate

Unlock the Latest in Real Estate

News, Infographics, Blogs & More! Delivered to your inbox.